Complete Edition: Displacement · Brand Wars · Economics · 12 Point-of-View Analysis

A data-driven intelligence report on how AI is restructuring the marketing profession, brand dynamics, consumer behaviour, and the global economics of attention.

TABLE OF CONTENTS

About This Report

— Executive Summary

— About AJ&VG Media

Part 1 — Core Intelligence

I Global AI Marketing Adoption: By the Numbers

II How Marketers Use AI: Global Use-Case Distribution

III Marketer Displacement: Who, How Many, and When

IV The Product Explosion & the Brand Wars

V The New Marketing Economics

Part 2 — 12 Critical Points of View

VI The Consumer Point of View

VII The SMB & Small Business Point of View

VIII The Regulatory & Policy Point of View

IX The Creative & Cultural Point of View

X The Ethics & Trust Architecture Point of View

XI The Talent Pipeline & Education Point of View

XII The Agency Business Model Point of View

XIII The Psychological & Human Capital Point of View

XIV The Geopolitical & Currency Point of View

XV The Platform & Distribution Point of View

XVI The Founder & Personal Brand Point of View

XVII The Measurement & Attribution Point of View

Synthesis & Conclusion

— Integrated 12-POV Synthesis

— The Five Strategic Imperatives

— The Evolving Role of the Marketer (Timeline)

— Who Wins, Who Loses

EXECUTIVE SUMMARY

Global advertising spend crosses $1 trillion for the first time in 2026. AI adoption among marketers reaches 88% daily usage. And yet — the profession is fracturing. This report presents the most comprehensive analysis available of three interlocking crises reshaping marketing globally: the displacement of human marketing labour, the collapse of brand differentiation in an AI-saturated product landscape, and the rewiring of marketing economics that follows.

This complete edition brings together both macro intelligence and 12 distinct points of view — consumer, SMB, regulatory, creative, ethical, educational, agency, psychological, geopolitical, platform, personal brand, and measurement — into a single unified intelligence framework. Each section is supported by the latest global research, statistics, and original analysis from AJ&VG Media.

| 88% Marketers using AI daily Up from 29% in 2021 | 65% Marketing tasks replaceable Anthropic research index | $1.14T Global ad spend 2026 First trillion-dollar year | 43% AI-skills wage premium Up from 25% one year ago |

| ~21M Marketing roles at risk Of 32M global workforce | 75% Measurement approaches failing IAB State of Data 2026 | 800% FDE job posting spike Jan–Sep 2025, Indeed/FT | 63% Vibe coding users are non-devs Marketers, PMs, founders |

| “Marketing is not dying — it is bifurcating. The total economic value of marketing increases. The number of people needed to produce that value decreases sharply. The concentration of value accelerates toward the AI-fluent, systems-thinking marketer.” — AJ&VG Media Analysis, April 2026 |

ABOUT AJ&VG MEDIA

AJ&VG Media is a Top 10 Marketing Consulting Firm (CIOReview India) with offices in Bengaluru and Dubai. We operate at the intersection of marketing strategy, AI systems, and software engineering — serving growth-stage tech companies across India and the GCC as Fractional CMOs, growth partners, and marketing intelligence architects.

Our Founder & CEO Ajeesh Nair operates as a “Creative Technologist” — a CMO with over two decades of B2B marketing experience who also engineers production-grade software. This dual capability is the foundation of the “CMO Who Codes” positioning and underpins AJ&VG Media’s unique ability to bridge strategic marketing and technical AI execution.

Chapter I

GLOBAL AI MARKETING ADOPTION: BY THE NUMBERS

The adoption of AI in marketing has moved from optional to universal in under four years. The global AI marketing market expanded from $12.05 billion in 2020 to $47.32 billion in 2025 — a 293% increase. It is projected to reach $107.5 billion by 2028 at a 36.6% CAGR. This is not incremental growth; it is a structural industry transformation.

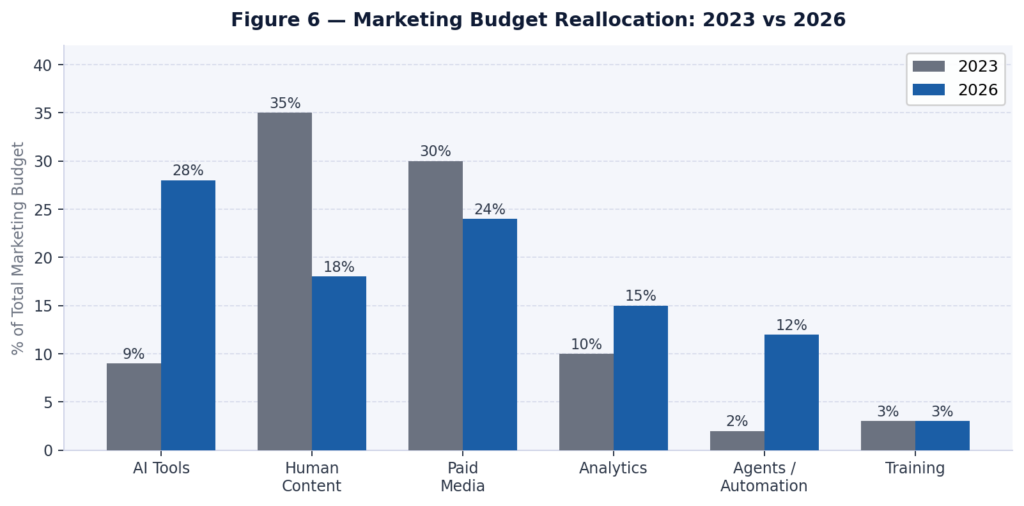

| $47B AI marketing market 2025 → $107.5B by 2028 | 76% Global business AI adoption Up from 29% in 2021 | 72% Orgs using AI for content Global, all sectors | 9% Budget to AI tools (2023) Now 28% by 2026 |

Regional Adoption Leaders

| Country / Region | AI Marketing Adoption | Primary AI Focus | Growth Trajectory |

| United States | 61% | Full-stack: content, paid, agents, analytics | $74B market, 26.95% CAGR through 2031 |

| China | 58% | GenAI content, e-commerce AI, WeChat automation | State-backed; high-scale platform AI |

| United Kingdom | 47% | Brand content, regulatory-aware AI | Strong agency AI investment |

| India | Fast-growing | 12% of global AI content editing | SMB AI adoption leading globally |

| UAE / GCC | High intent | Gov-backed AI, retail, fintech | Net positive employment; AI-first policy |

| APAC (Singapore, ANZ) | 40.7% vibe coding | Agency AI, tool building | Fastest-growing region 19.2% QoQ |

| Germany / EU | Moderate, GDPR-constrained | B2B analytics, compliant AI | Regulation creating differentiation |

Chapter II

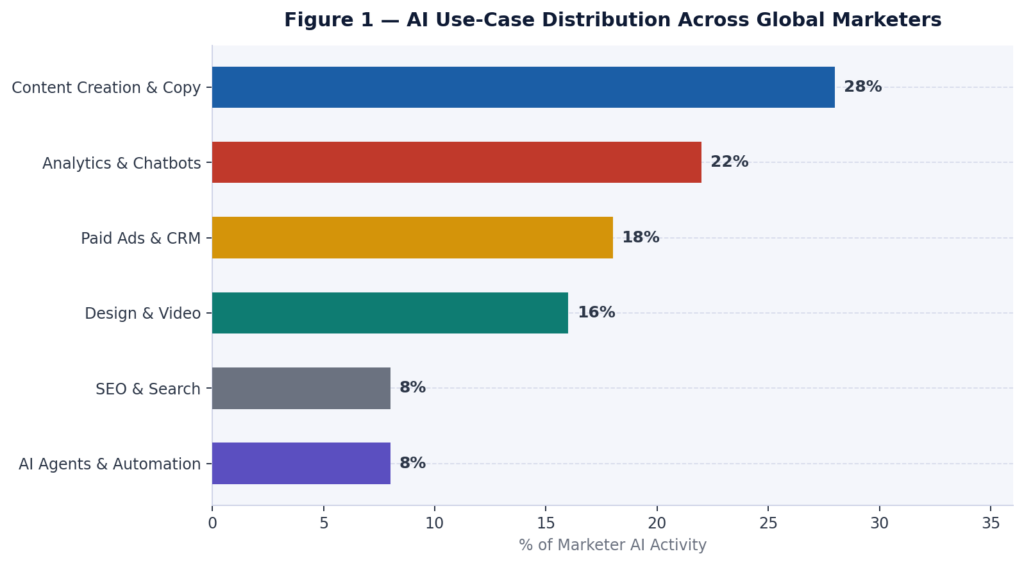

HOW MARKETERS USE AI: GLOBAL USE-CASE DISTRIBUTION

AI usage across marketing is not uniformly distributed. Content creation dominates — but the fastest-growing and most transformative category is agentic AI. Understanding the distribution reveals both where displacement is most acute and where the highest-leverage opportunities exist.

| 80% Generate short articles with AI Top content use case globally | 75% Use AI for video & image creation Design category surging | 56% Use AI for customer service Most common overall use case | 19.6% Planning AI agent deployment Growing fastest YoY |

Content Category Breakdown — Where AI Writing Actually Goes

| Content Category | AI Adoption % | Key Tools | Risk Level (displacement) |

| Short articles & blog posts | 80% | ChatGPT, Jasper, Claude | Very high |

| Content outlining & briefs | 73% | Claude, ChatGPT | High |

| Video scripts | 71% | ChatGPT, Claude, Jasper | High |

| SEO optimisation | 67% | SurferSEO, Semrush AI | High |

| Email & newsletters | 51% | HubSpot AI, Klaviyo | Medium-high |

| Social media posts | 49% | Buffer AI, Sprout AI | Medium-high |

| Image & design generation | 41% | Midjourney, DALL-E, Canva AI | Medium |

Chapter III

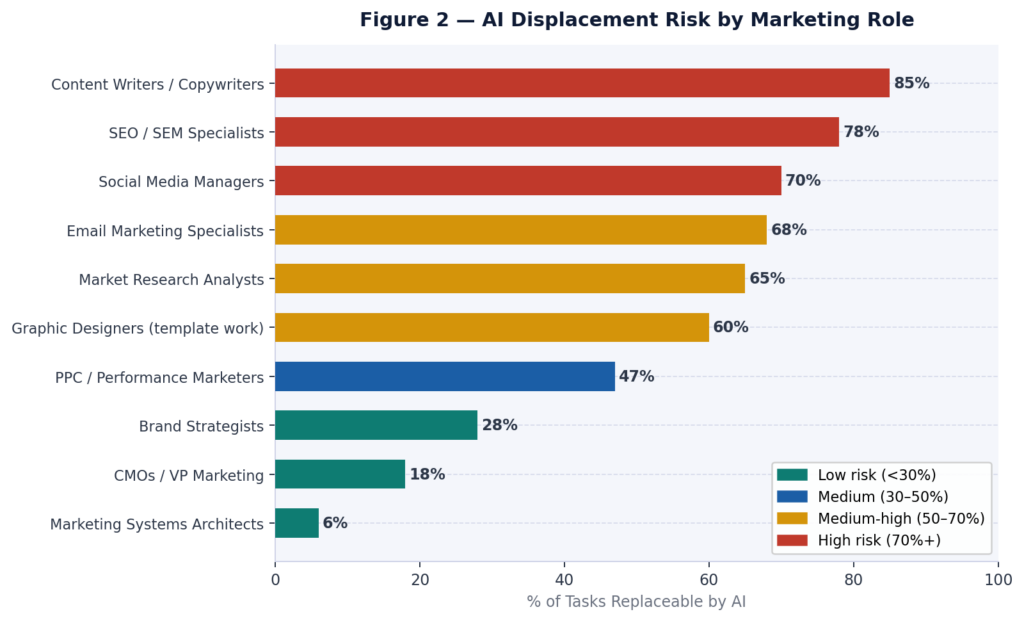

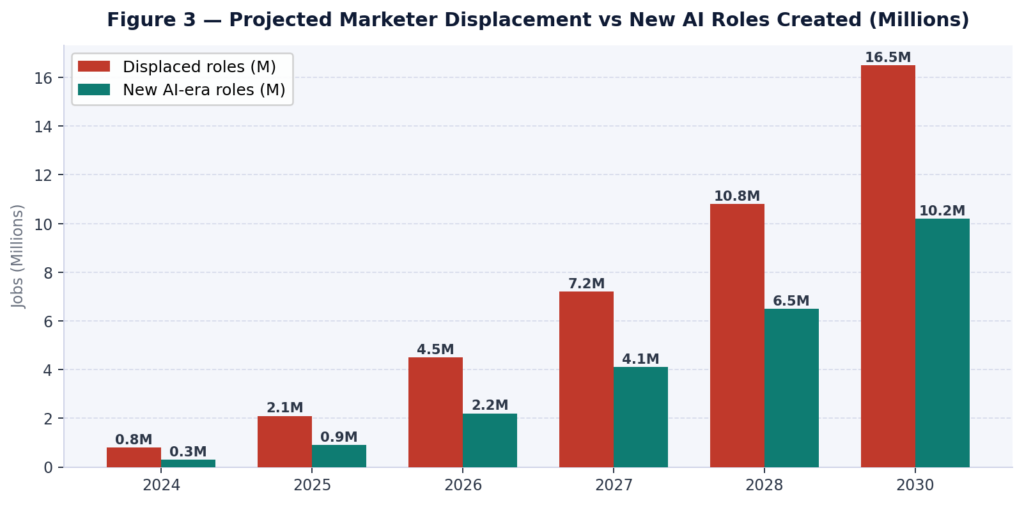

MARKETER DISPLACEMENT: WHO, HOW MANY, AND WHEN

The displacement of marketing professionals by AI is not a future threat — it is a present, measurable, and accelerating reality. Anthropic’s research ranked marketing specialists fifth on its list of 800 occupations most exposed to AI displacement. 65% of tasks performed by marketing professionals are eventually replaceable with AI operations.

| ~32M Global marketing workforce 2026 estimate | 65% Tasks AI can replace Anthropic displacement index | ~21M Roles at high risk Of 32M globally by 2030 | −14% Junior marketer hiring drop vs 2022 baseline, US data |

| The Hidden Displacement: AI is not just firing people — it is suppressing hiring. Marketing jobs in the US fell 7% YoY and 15% QoQ in Q2 2025. The junior analyst who once synthesised research, built decks, and wrote first drafts is simply no longer being hired. The organisation discovers it did not need those roles anyway. This soft displacement is harder to see and far harder to reverse. |

Country-Wise Displacement Breakdown

| Country | Roles at Risk | Primary Exposure | Buffer Factors |

| United States | ~3.2M | Content, SEO, social media — all junior tiers | Fastest to create new AI roles |

| India | ~2.8M | BPO-adjacent content marketing; large workforce | SMB AI adoption growing fast; new AI roles emerging |

| United Kingdom | ~420K | Creative agencies; media buyers; content teams | Agency consolidation managing timing |

| China | Transition | Content farms automated; platform roles evolving | State-directed retraining programmes |

| Germany / EU | ~310K | B2C marketing; admin & analytical roles | GDPR and AI Act slow automation speed |

| UAE / GCC | Low | Small base workforce | Gov AI programmes focus on augmentation |

| The Wage Gap is Accelerating: Marketing professionals with AI skills command a 43% wage premium as of 2026 — up from 25% just one year earlier. In concrete terms, approximately $18,000 less annually for non-AI marketers today. This gap will widen to 60%+ by 2028 without intervention. |

Chapter IV

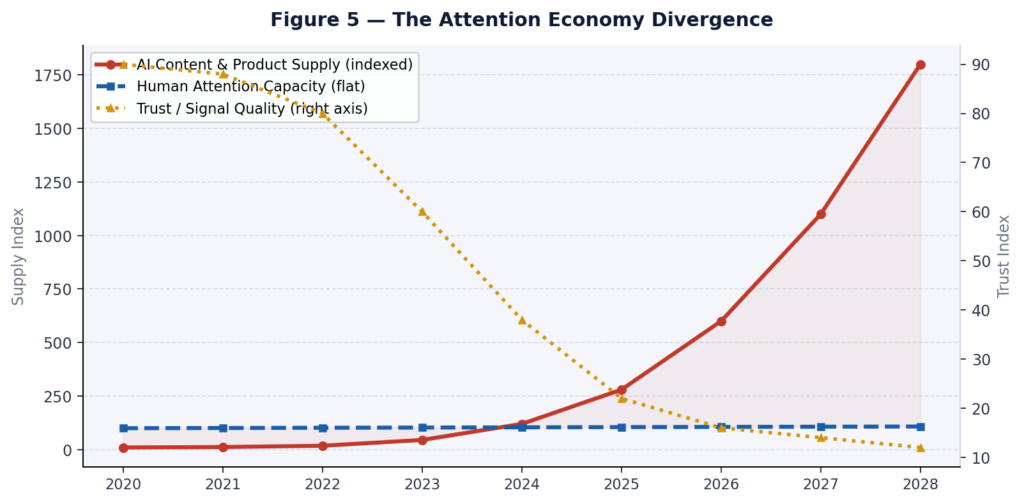

THE PRODUCT EXPLOSION & THE BRAND WARS

When AI reduces the time and cost to build and launch products by 5–10x, the supply side of every market floods. 40% of new SaaS MVPs in 2026 are being built primarily via AI-assisted development. The market is experiencing its most significant product explosion in history — and with it, the most acute brand differentiation crisis.

| 40% New SaaS MVPs via AI coding 2026 projection | $50B+ AI startup VC in 2024 Venture capital deployed | 80% No click on AI overview appearances Moloco / BCG AI Disruption Index | 75% Consumers trust AI to find better deals Than they can themselves |

| “Slop” was named a 2025 word of the year for a reason. When every brand publishes AI-generated content, everything trends toward the median — indistinguishable, forgettable, trusted by no one. AI systems themselves then struggle to identify who actually knows what they are talking about. This is the homogenisation crisis — and it is already here. |

Brand Disruption Index — Vertical Exposure

| Brand Vertical | Disruption Level | Primary Threat Vector | Strategic Moat |

| E-commerce / Retail | EXTREME 92% | AI agents replacing discovery; no-click journeys | Loyalty data; owned community |

| Financial Services | VERY HIGH 85% | AI comparison tools disintermediating brand | Regulatory trust; relationship capital |

| B2B SaaS | HIGH 80% | Product explosion saturating every niche | Proprietary data; deep integration |

| Media / Content | HIGH 78% | AI flooding every channel; signal collapse | Original IP; editorial voice; community |

| Consumer Goods / FMCG | MEDIUM-HIGH 65% | Private label AI insurgents | Brand heritage; distribution moats |

| Luxury / Heritage | LOWER 28% | Synthetic luxury alternatives | Scarcity; provenance; human craft story |

| Local / Community | LOW 18% | Generic AI competing with local | Physical relationships; geographic trust |

| “Strategy and brand differentiation will matter again because everything else is rapidly commoditising. The era of hedging with endless AI experiments is ending. Experimentation is no longer a strategy.” — Adweek, 10 AI Marketing Trends for 2026 |

Chapter V

THE NEW MARKETING ECONOMICS

The financial architecture of marketing is being completely reconstructed. Global ad spend crossing $1 trillion is evidence of the industry’s continued economic importance. But internally, every input cost is collapsing and every output expectation is rising simultaneously.

| $1.14T Global ad spend 2026 First trillion-dollar year | 68.7% Digital share of ad spend Up from 64% in 2024 | 71.6% Ad spend algorithm-managed 2026 global estimate | 28% Budget to AI tools (2026) Up from 9% in 2023 |

The Cost Structure Revolution

| Metric | Traditional | AI-Enabled | Change |

| Content cost per piece | $300–$800 | 4.7x cheaper with AI | −79% cost |

| Video production per minute | $4,500 | $400 (AI-generated) | −91% cost |

| Campaign launch time | Weeks of production | 75% faster | Structural shift |

| Marketing overhead | Baseline | −10.8% (McKinsey CMO Survey) | Proven across 3 surveys |

| AI-skilled marketer salary | Market rate | +43% premium vs peers | Up from 25% YoY |

| Annual AI tool spend (avg team) | N/A | $12,500 per team | Fastest-growing budget line |

| The ROI Paradox: 84% of CMOs say ROI is now the primary budget-allocation criterion. Yet the share of CMOs whose CEO and CFO support long-term brand investment fell to 69% from 80% year-on-year. Performance marketing is eating brand marketing’s budget — exactly at the moment when brand differentiation matters most. This is the most dangerous misalignment in marketing today. |

| “Crossing the trillion dollar threshold signals a structural shift in how growth is created. Media is now the front door to every brand and the most powerful system for driving relevance, creativity and value at scale.” — Will Swayne, Global Practice President, dentsu Media |

PART TWO

12 CRITICAL POINTS OF VIEW

A 360-degree analysis of the forces reshaping marketing from every angle:

Consumer · SMB · Regulation · Culture · Ethics · Talent Agency Model · Human Capital · Geopolitics · Platforms · Founder Brands · Measurement

Chapter VI

THE CONSUMER POINT OF VIEW

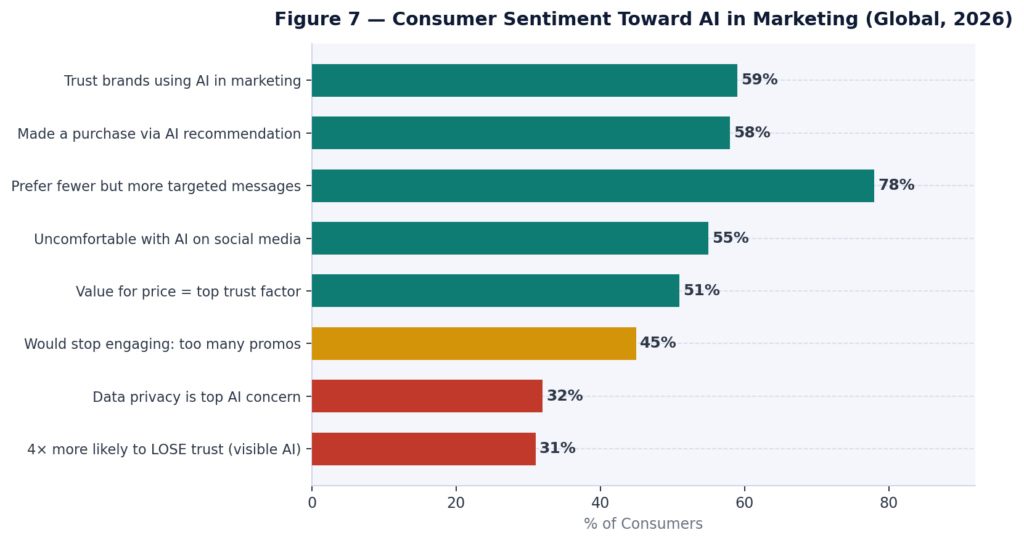

The consumer is the silent protagonist of the entire AI marketing drama. The picture that emerges from 2025–2026 research is nuanced: consumers simultaneously want the personalisation AI enables, yet are significantly more likely to lose trust when they visibly detect AI in brand communications.

| 59% Trust brands using AI When execution is relevant | 4x More likely to LOSE trust When AI content is visible | 71% Abandon irrelevant AI experiences Twilio global study, 2025 | 78% Prefer fewer but targeted messages Optimove Consumer Fatigue Report |

Among Adobe’s global study of 4,000 consumers: 51% say value for price is the top trust factor — ahead of brand reputation, consistency, and values. Only 18% say they purchase exclusively from brands they fully trust when cheaper alternatives exist. And nearly half (45%) will stop engaging with a brand if they receive too many promotions, even if the content is personally relevant.

| The Invisible Trust Tax: Americans believe only 41% of online content is accurate, factual, and human-made. Three-quarters say their trust in the internet is at an all-time low. Brands operating in this environment are not just competing for attention — they are competing against a baseline assumption of inauthenticity. |

| “When people feel they’re being talked at by a machine, they don’t feel valued. Once that happens, it’s difficult to rebuild that trust.” — Michelle Taves, VP Group GM Data & Marketing, Porch Group Media (2026) |

Chapter VII

THE SMB & SMALL BUSINESS POINT OF VIEW

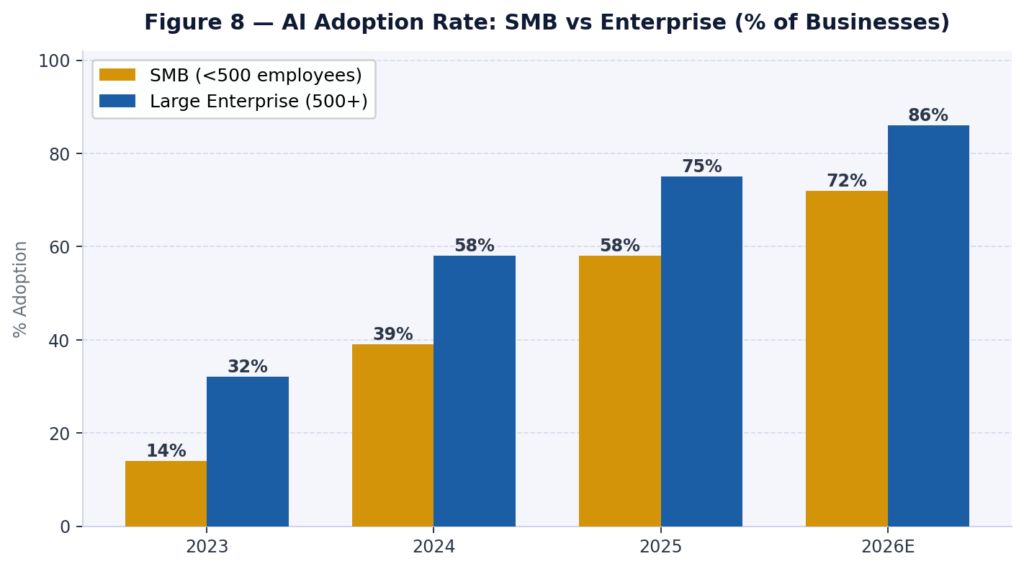

The 750 million small businesses globally represent the most overlooked story in AI marketing. For them, AI is simultaneously the greatest competitive equaliser in history — and a force that can erase hard-won local differentiation overnight.

| 91% SMBs with AI report revenue boost Salesforce SMB Trends, 2025 | 58% SMBs now use generative AI Up from 40% in 2024 | 83% Growing SMBs adopted AI vs 55% of declining businesses | 82% Very small firms: “AI not relevant” Education gap, not reality |

| The SMB Survival Signal: 83% of growing SMBs have adopted AI compared to just 55% of declining businesses. The correlation between AI adoption and business trajectory has become the clearest leading indicator of SMB health in 2026. AI adoption is no longer a growth strategy — it is a survival signal. |

Chapter VIII

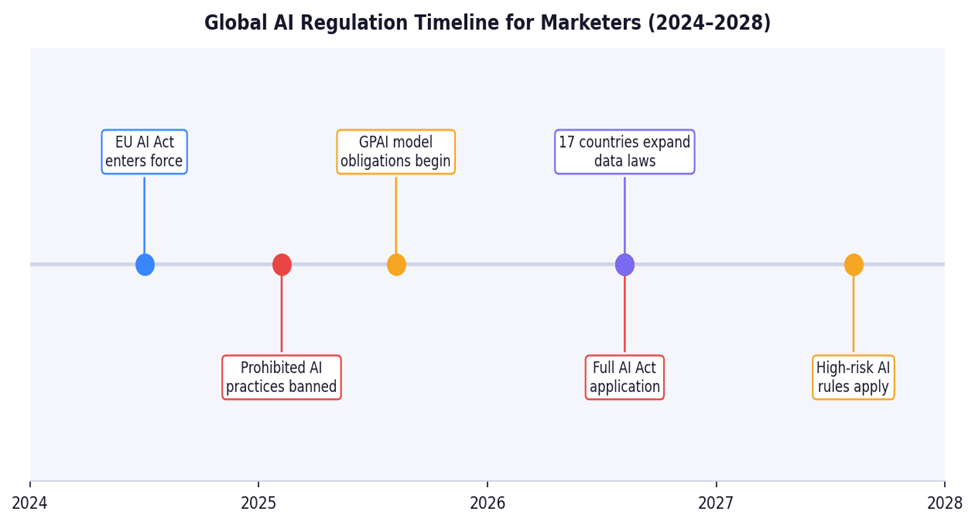

THE REGULATORY & POLICY POINT OF VIEW

2026 is the year AI regulation stops being a future concern and becomes a present operational reality. The EU AI Act enters full application on August 2, 2026. 17 countries enacted or expanded data laws in 2025 alone. $2.1 billion in regulatory fines related to AI misuse were issued globally in 2025 — a 7x increase from 2023.

| €35M Max EU AI Act fine Or 7% of global annual turnover | Aug 26 EU AI Act full application Transparency rules now enforceable | 17 Countries expanded data laws (2025) Global regulatory wave | 42% Enterprises adjusted AI for EU Act Gartner, early 2026 |

| Marketing AI Type | Risk Category | Key EU Obligation | Live From |

| Customer chatbots | Limited risk | Must disclose AI identity at first interaction | Aug 2026 |

| AI-generated content | Limited risk | Machine-readable marking; human-readable disclosure | Aug 2026 |

| Synthetic influencers / deepfakes | Limited risk | Clear labelling as artificially generated | Aug 2026 |

| Personalisation engines | Minimal risk | No specific obligation; GDPR applies | Ongoing |

| AI-targeted advertising | Minimal risk | No specific AI Act obligation | Ongoing |

| Emotion recognition | High risk | Full risk management + human oversight | Aug 2027 |

| The Compliance Dividend: 37% of UK marketers who overhauled their AI approach after the EU AI Act reported increased consumer trust. Brands that make transparency a brand value — not a legal checkbox — are finding it becomes a genuine competitive differentiator. |

Chapter IX

THE CREATIVE & CULTURAL POINT OF VIEW

When creativity — the act of making something original, emotionally true, and culturally resonant — is reduced to a latency-optimised generation pipeline, something is lost that cannot be measured in CTR. The marketing profession is in danger of optimising its way out of cultural relevance.

AI excels at mimicry: it produces content that resembles great creative work in every measurable dimension. The problem is that culture does not progress through resemblance. Movements, moments, and brand mythologies are created through risk, surprise, and specificity. An AI trained on all existing creative output will produce the weighted average of everything that has already worked — which is, by definition, never new.

| “A lot of the output is trending toward the median. It’s about pulling against the median because all of the content is merging to look very, very similar.” — Taryn Crouthers, CEO, Spcshp (Adweek, January 2026) |

| The Creative Paradox: By making average creative free and instant, AI dramatically raises the value of genuinely distinctive creative. As AI floods every channel with polished-but-interchangeable content, the brands that invest in real creative risk — the discomforting campaign, the artistically courageous work — will stand out with disproportionate effect. The creative brief has never mattered more than it does today. |

Chapter X

THE ETHICS & TRUST ARCHITECTURE POINT OF VIEW

The AI era has not created new ethical problems in marketing — it has massively amplified existing ones and created several genuinely new ones. The profession that defines how brands communicate has a responsibility that extends far beyond legal compliance.

| 29% Companies with AI ethics committee Only 29% have governance | $2.1B AI regulatory fines globally (2025) 7x increase from 2023 | 53% Consumers: AI support = privacy risk Qualtrics global study | 46% Share data with transparent brands vs 39% trusting data use today |

| Ethical Issue | The Problem | Status |

| Synthetic personas & AI influencers | Undisclosed AI identities deceive consumers about endorsements | No universal standard; EU Act applies Aug 2026 |

| Hyper-personalisation vs manipulation | The line between helpful relevance and psychological exploitation | Largely unregulated; brand ethics driven |

| Algorithmic bias in targeting | AI ad systems systematically exclude protected groups | US enforcement cases emerging |

| AI content disclosure | Consumers have no reliable way to know content origin | EU Act mandates disclosure Aug 2026 |

| Ads in AI assistants (ChatGPT Feb 2026) | Most trusted AI interface now has commercial incentive to recommend | Unregulated; industry-defining moment |

| OpenAI’s February 2026 rollout of advertising inside ChatGPT is the defining ethical moment of the AI marketing era. For the first time, the most trusted AI information interface has a commercial incentive to recommend paid products. The trust contract between AI and user is being renegotiated in real time — and marketers are at the centre of that negotiation. |

Chapter XI

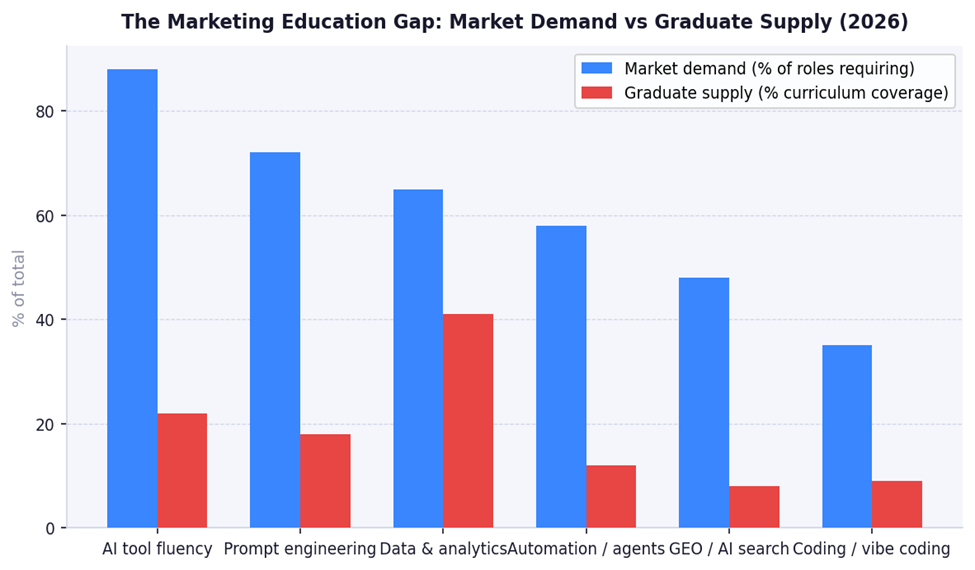

THE TALENT PIPELINE & EDUCATION POINT OF VIEW

Universities, business schools, and marketing academies are producing graduates with 2019 skill sets for a 2026 job market. Only 17% of marketing professionals have received comprehensive, job-specific AI training — despite 88% using AI tools daily. This is not an individual failure; it is a structural one.

| 17% Marketers with proper AI training Despite 88% daily AI usage | 43% Higher success with AI education Companies investing in training | 6% Fully embedded AI in workflows Supermetrics 2026 study | 80% Feel pressure to adopt AI But lack formal training |

| The Cascade Effect: The talent gap compounds the displacement crisis. Organisations that cannot find AI-fluent marketers are replacing human roles with AI systems rather than upskilling humans to work alongside AI. The absence of training infrastructure accelerates the very displacement it could prevent. |

Chapter XII

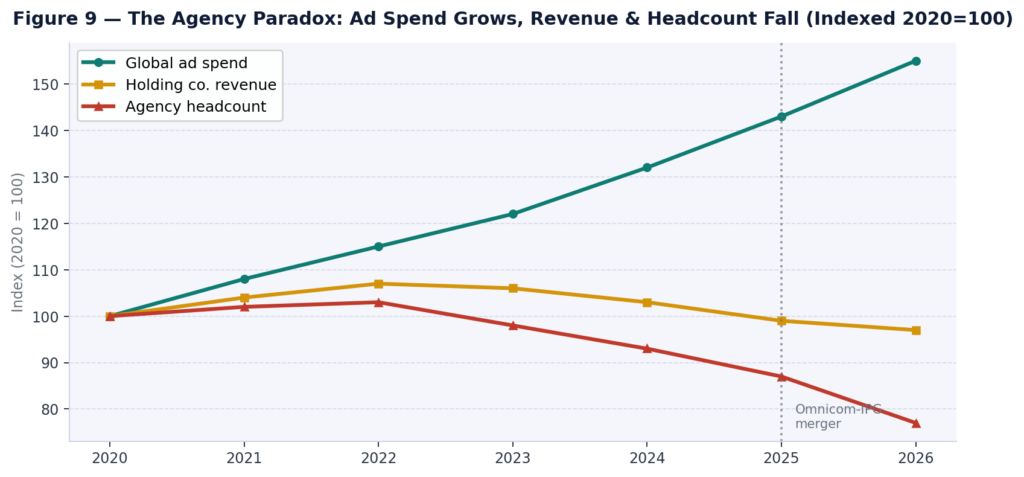

THE AGENCY BUSINESS MODEL POINT OF VIEW

The advertising industry reached an extraordinary milestone in 2026: global ad spend surpassed $1 trillion for the first time. And yet, major holding companies saw their revenues fall 1.2% year-over-year while that same ad spend grew 8.6%. This is the agency paradox — and it is the structural consequence of AI removing the labour arbitrage the agency model was built on.

| 60% Senior marketers cut agency spend Direct result of AI — Typeface 2025 | −8% Average agency headcount cut 2025 Forrester: 15% projected 2026 | $13.5B Omnicom-IPG merger (Nov 2025) 4,000 jobs eliminated | 2028 “Double profits, halve people” Global holding co CEO, Forrester |

| Agency Type | AI Impact | Survival Strategy |

| Large holding companies | Revenue declining despite spend growth; 8%+ headcount cuts | Consolidation, AI platform investment, data differentiation |

| Mid-size independents | Squeezed from above (holdcos) and below (AI-native boutiques) | Niche specialisation; outcome-based pricing; owned IP |

| AI-native boutiques | Growing rapidly; lean by design | Speed, AI fluency, transparent attribution |

| Fractional CMO / consulting | Fastest-growing segment globally | Senior strategy + AI execution = premium value |

| In-house teams | Expanding as brands reclaim capabilities | AI tooling reducing headcount needed for same output |

| For AJ&VG Media: the Fractional CMO and AI-native consulting model is positioned precisely at the intersection of all three disruption vectors simultaneously — agency model collapse, in-housing acceleration, and AI capability democratisation. The market is structurally moving toward exactly what AJ&VG Media offers. |

Chapter XIII

THE PSYCHOLOGICAL & HUMAN CAPITAL POINT OF VIEW

60% of employees fear that generative AI will increase stress and burnout. What the data does not capture is the identity crisis experienced by a generation of professionals who built their self-worth around a craft that is now commoditised. Marketing attracts people who derive meaning from creative expression. The psychological toll of that craft becoming automated deserves more than a footnote.

| 60% Employees fear AI increases burnout 2026 trend data | 70% Non-AI marketers: higher burnout Competing against AI-enabled peers | 2% US voluntary quit rate Lowest in a decade — fear of job loss | 40% Employers choose automation over upskilling SHRM Automation/AI Survey 2025 |

| The Junior Pipeline Collapse: AI is specifically displacing entry-level roles at the moment when an entire generation of aspiring marketers should be building foundational career capital. The long-term consequence is a skill gap not just in AI fluency, but in the analogue fundamentals — client relationships, strategic instinct, editorial judgment — that only come from doing the junior work. |

Chapter XIV

THE GEOPOLITICAL & CURRENCY POINT OF VIEW

The global marketing economy operates on AI tools built predominantly by US companies. This concentration of AI infrastructure in two geopolitical poles — US and China — has profound implications for every marketing team in every country that sits outside those poles. The dollar-denominated AI economy creates a structural cost asymmetry that the democratisation narrative obscures.

| 38% US share of global AI investment vs China 26%, EU 18% | $301B Total global AI spend 2026 IDC Worldwide AI Spending Guide | 59% India SMBs implementing AI solutions Leads SMB AI adoption globally | 19.2% APAC quarterly AI market growth Fastest-growing region globally |

| Market | AI Marketing Opportunity | Key Risk | Strategic Priority |

| India | Largest English AI content market outside US; 59% SMB AI adoption | Talent displacement in content workforce | Upskilling + AI-native content strategy |

| UAE / GCC | Gov-backed AI programmes; high enterprise budgets | Dollar-denominated tool costs; regulatory ambiguity | AI governance advisory + execution |

| Southeast Asia | APAC fastest-growing; 40.7% vibe coding adoption | Fragmented regulatory environment | Platform-specific AI strategy |

| EU / UK | Premium trust market; compliance creates differentiation | Heavy regulatory compliance costs | Compliance-as-brand-strategy |

Chapter XV

THE PLATFORM & DISTRIBUTION POINT OF VIEW

The platform and distribution landscape is experiencing its most dramatic restructuring since the advent of programmatic advertising. AI agents are beginning to intermediate between brands and consumers at every stage of the buyer journey — and the major platforms are racing to control that intermediation layer.

| 14.1% Retail media growth 2026 Fastest-growing digital channel | −3.8% Linear TV ad spend decline Structural, not cyclical | 80% ChatGPT share of AI referral traffic Conductor 2026 benchmark | 4.4x AI citation traffic conversion rate vs traditional organic search |

| GEO is now a media channel. Being cited by ChatGPT, Claude, Perplexity, and Google AI Overviews is quantifiable media exposure with a conversion rate 4.4x higher than traditional organic. The first marketing teams to build systematic GEO programmes — with dedicated budgets, content strategies, and citation measurement — will capture an asymmetric first-mover advantage in the highest-converting discovery channel of the decade. |

Chapter XVI

THE FOUNDER & PERSONAL BRAND POINT OF VIEW

In a world where every brand can generate infinite content at zero marginal cost, the one thing AI cannot replicate is a real human being with a distinctive perspective, proven expertise, and genuine relationships. Founder-led personal brands and thought leadership are not just marketing tactics — they are the most structurally defensible brand assets in the AI era.

| 18% Creator/influencer ad spend growth $10B+ market in US alone | 61% Brands increasing creator investment Unilever scaling to 300K creators | 4.4x AI citation traffic conversion Personal brands cited most often | 43% AI skills wage premium Max leverage = AI fluency + expertise |

The CMO Who Codes: A Category Definition

The intersection of senior marketing domain expertise, AI systems fluency, and software-building capability represents a genuinely new professional category — one that has no historical precedent and that the market has not yet fully priced. The person who can architect marketing intelligence systems, evaluate AI output with expert judgment, and build custom tools while also having two decades of brand-building instinct is not competing with anyone. They are creating a new category.

| “The revolution doesn’t belong to the coders. It belongs to the Orchestrators. In 2026, the most valuable skill isn’t knowing how to write a for-loop. It’s having the taste to know when a feature feels right and the architectural literacy to guide agents toward a coherent vision.” — Vibe Coding Stack Analysis, Medium (January 2026) |

Chapter XVII

THE MEASUREMENT & ATTRIBUTION POINT OF VIEW

Marketing has been measured by the click for three decades. The click is disappearing. AI Overviews answer queries without clicks. ChatGPT recommends products without clicks. Consumers research through AI interfaces that leave no trackable signal in Google Analytics. The measurement architecture of modern marketing is built for a world that no longer exists.

| 75% Measurement approaches underperform IAB State of Data 2026 | 58% Searches are zero-click AI overviews + featured snippets | 40% Struggle to prove cross-channel ROI Supermetrics 2026 study | 19% Track AI-specific KPIs Despite 74% using AI in content |

| Old Metric | Why It Broke | New Metric 2026 | What It Measures |

| Organic traffic | AI Overviews absorb 20–35% of clicks | Share of Model (SOM) | Brand citation frequency in LLM responses |

| Last-click attribution | Multi-touch journeys invisible to last-click | Pipeline-influenced revenue | Deals where content touched buyer journey |

| CTR from search | Zero-click searches now 58%+ of queries | Self-reported attribution | “How did you hear about us?” at every form |

| Platform ROAS | Black-box optimisation; walled garden bias | Incrementality testing | Causal lift vs holdout group |

| Page views | AI-influenced visits arrive through other channels | Intent signal quality | Buyer intent depth at conversion point |

| The single highest-return measurement investment in 2026: Add a free-text “How did you hear about us?” field to every form. Companies implementing self-reported attribution consistently discover that 30–50% of qualified leads cite channels invisible to standard analytics — including ChatGPT recommendations, LinkedIn DMs, and podcast episodes. |

SYNTHESIS & CONCLUSION

The Integrated View

INTEGRATED 12-POV SYNTHESIS

Across all 12 points of view, a unified narrative emerges. AI is not disrupting marketing from the outside — it is restructuring it from within. The disruption is not primarily technological. It is simultaneously economic, cultural, psychological, regulatory, and geographic. The professionals, brands, agencies, and businesses that navigate this transition successfully will be those that hold all 12 lenses in view at once.

| Point of View | Core Insight | Urgency |

| Consumer | Trust is won through relevant execution, lost through visible AI. 4x trust penalty for detected AI. | Critical |

| SMB | AI is the equaliser. Non-adoption is the new competitive disadvantage. 83% of growing SMBs use AI. | High |

| Regulation | EU AI Act full application August 2026. Disclosure, labelling, and transparency are now law. | Critical |

| Creative & Cultural | AI commoditises average creative; dramatically raises premium for genuinely original work. | High |

| Ethics | Only 29% of companies have AI ethics governance. ChatGPT ads redraw the trust contract. | High |

| Talent Pipeline | 17% proper training despite 88% daily use. Education system 5 years behind the market. | High |

| Agency Model | Ad spend grows, agency revenue falls. Labour arbitrage model is structurally over. | Critical |

| Human Capital | 60% fear burnout. Identity crisis among creative professionals is real and compounding. | Medium |

| Geopolitics | US-dollar AI economy creates asymmetric cost burden. India and GCC are strategic opportunities. | Medium |

| Platform & Distribution | Retail media and GEO are fastest-growing channels. Linear TV and print dying structurally. | Critical |

| Founder / Personal Brand | Human expertise with verifiable track record is the scarcest and most valuable asset in AI era. | Critical |

| Measurement & Attribution | 75% of measurement approaches underperform. The click is disappearing. New KPIs required. | Critical |

THE FIVE STRATEGIC IMPERATIVES

Based on the integrated analysis across all 16 chapters, these are the five non-negotiable strategic priorities for marketing leaders in 2026 and beyond:

- Build GEO into your brand strategy now — be cited by AI systems, not just found by search engines. Traffic that arrives from AI citations converts at 4.4x the rate of traditional organic search.

- Invest in verifiable expertise — proprietary data, original research, non-replicable domain authority that AI cannot fabricate on demand.

- Develop AI fluency at every level — close the 43% wage gap before it becomes 60%. Upskilling is the highest-return investment available in any marketing budget.

- Resist performance-only budget pressure — brand equity is the long-term moat that AI cannot replicate. The ROI paradox is the most dangerous misalignment in marketing today.

- Build trust infrastructure — 62% of consumers globally say trust is their decisive purchase factor. The brands that survive are not those that produce the most — they are those that mean the most.

THE EVOLVING ROLE OF THE MARKETER: 2020–2030

| Era | Marketer Identity | Primary Skill | AI Relationship |

| 2020–2022 | Content executor | Writing, design, briefing agencies | AI is a grammar checker; peripheral tool |

| 2022–2024 | AI-assisted creator | Prompting, editing, repurposing AI output | ChatGPT, Jasper, Midjourney enter the stack |

| 2024–2025 | Tool builder | Vibe coding calculators, landing pages, automation scripts | 63% of vibe coding users are non-developers |

| 2025–2026 | Agent orchestrator | Defining goals; designing systems; evaluating output | 19.6% building AI agents; FDE roles up 800% |

| 2026–2028 | Eval + governance layer | QA of AI output; brand safety; strategic oversight | 80% of teams will deploy autonomous AI systems |

| 2028–2030 | Strategic orchestrator | Business context, brand soul, audience empathy | AI executes everything; human defines meaning |

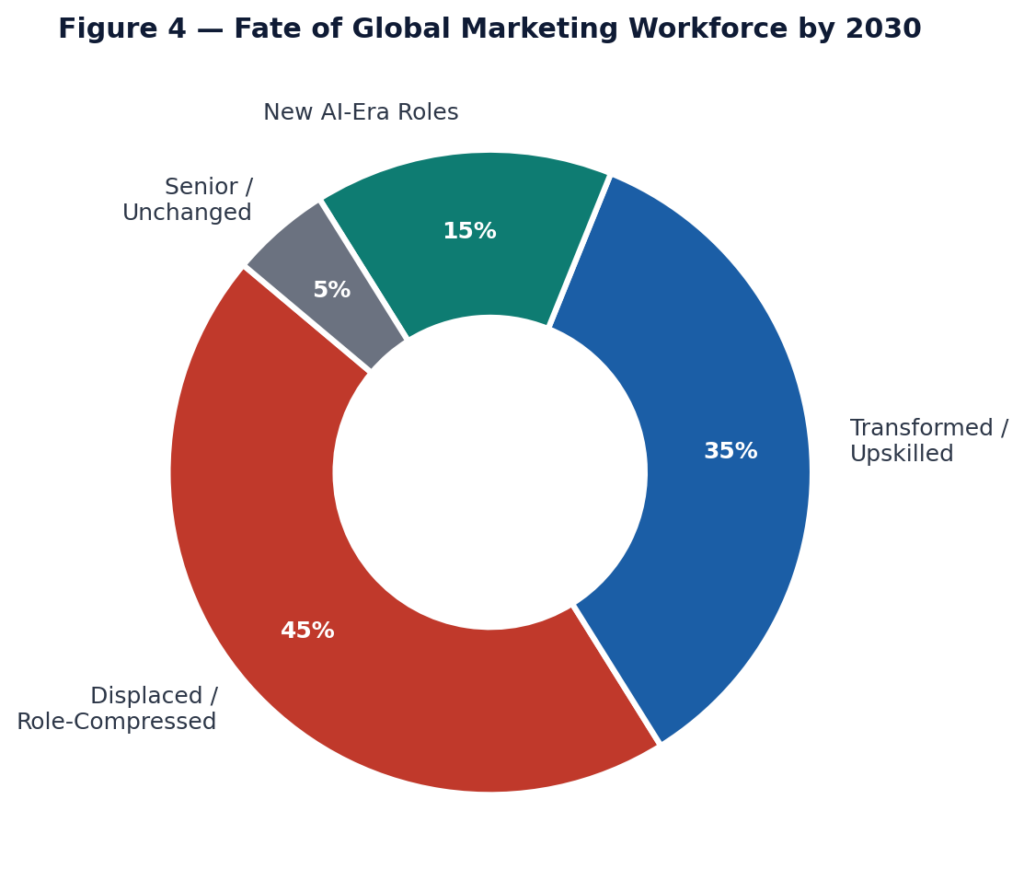

WHO WINS, WHO LOSES

| WHO LOSES The Commodity Marketer Operates as a content producer, task executor, or channel manager. Does not understand AI systems, cannot build tools, cannot architect workflows. Faces salary compression, role elimination, or outsourcing. Represents approximately 55–65% of the current global marketing workforce. | WHO WINS The Orchestration Strategist Combines deep domain expertise with systems thinking and AI fluency. Builds agents, evaluates outputs, architects trust infrastructure. Commands a 43%+ wage premium and grows with the market. The CMO Who Codes archetype — currently ~8–15% of marketers globally. This is where the market is moving. |

| THE FINAL MACRO INSIGHT Global ad spend crosses $1 trillion in 2026. Marketing is not dying — it is bifurcating. The total economic value of marketing increases. The number of people needed to produce that value decreases. The concentration of value in AI-fluent, systems-thinking marketers accelerates. The marketing economics equation has permanently shifted from headcount to leverage. The marketers who survive and thrive will not be those who adopted AI the fastest. They will be those who understood it most completely — its capabilities, its limits, its economics, its ethics, and its cultural consequences. |

{kind=link}